AFG Quarterly Index - Customer and Lender Landscape

Every quarter we release our index report which tells the story of recent mortgage buying trends in Australia. The report shows the lodgement activity of our national network of brokers and outlines the flows of business to the country’s leading lenders.

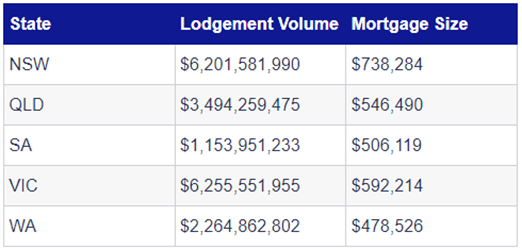

Lodgements and customers

AFG CEO David Bailey explained the results. “AFG recorded a drop in lodgement volume of 3.3% for the third quarter of the 2023 financial year,” he said. “This is 11.67% down on the corresponding period last year, however, lodgements remain consistently above pre-pandemic levels.”

“Investors continued to dip their toe back into the market, with Investment lodgements up 1% to 28%,” he said. “Despite many reports of First Home Buyers pulling back, they represented 12% of volume, a 1% increase in those taking their first steps into the housing market. This is a reflection of full employment still underwriting demand for home equity.” Refinancing was steady at 31% and Upgraders were down 1% to 38%. Average loan size dropped from $600,149 to $598,258 for the quarter and the national Loan to Value Ratio is up from 65.4% to 65.7%.

Lenders

“The extraordinary competition between the major banks for market share, including cashbacks on offer for new customers, has seen the major lenders once again take market share from their non-major rivals,” said Mr Bailey. “Major lender lodgements were up 2.2% to 61.8%, the highest level since the final quarter of 2020. This has been fuelled by the majors continuing to benefit from lower funding costs linked to the government’s Term Funding Facility, a lag in passing on deposit rate increases to customers, and the prevalence of subeconomic cash back offers.”

After a welcome pause this month in rate increases, homebuyers facing the impact of ten successive interest rate rises will be looking for ways to save. “The major banks’ customers often pay a ‘loyalty tax’ as lenders chase new customers with better rates and cashback offers, usually at the expense of their existing customers,” he said. “This will encourage customers to shop around, however, with competition in the home loan market continuing to be the domain of the major lenders, the restoration of an even playing field for non-major lenders is vital to ensure alternative lending options.”

“As markets factor in predictions of rate falls next year, the pricing of longer-term fixed rate products is beginning to reflect this expectation. This has in turn led to more borrowers choosing a Fixed Rate loan, with the share of those products rising from 4.8% to 5.6%,” he said. “This is the second consecutive quarter they have ticked up, albeit still well below long-term averages.”

Recommended Articles

Stay up to date with the latest updates

View all of the latest articles to help enable you to grow and succeed as a mortgage broker with AFG.

View all